By Penny Yi Wang for Medill News Service

In the past few years, consumers disillusioned with tight-fisted banks have jumped on the peer-to-peer lending bandwagon.

When the Great Recession hit, banks suffered big losses as borrowers defaulted on loans they had taken out during the economy’s long upturn. In response, lenders have drastically tightened their lending requirements. As a result, many borrowers with anything less than stellar credit now can’t qualify for traditional bank loans.

But non-wealthy Americans still need loans from time to time. And as bankers have turned stingy, borrowers have increasingly turned to alternative online lending platforms, such as Lending Club and Prosper Marketplace.

Both companies are prominent players in the rapidly growing field of “peer-to-peer” lending. Under the “P2P” format – which didn’t exist until Prosper and Lending Club were founded less than a decade ago – online companies pool money from investors and make loans to consumers. It’s a disruptive model that resembles Uber, in that it eliminates the intermediary – the bank – in the lending process.

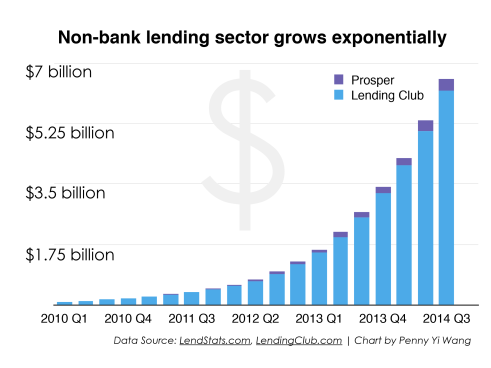

One of the biggest players in this field is the Lending Club, which recently filed for an initial public offering and just revised its per share estimates from $10-$12 to $12-$14 after meetings with potential investors around the nation.

The company’s current estimates for total funds that it could raise after its IPO is $808 million, and the company’s market capitalization would be around $4.3 billion, according to the company’s latest reports.

Institutions like hedge funds increasingly invest in loans to private sector businesses and individuals, according to fund managers.

In the Chicago region, investment companies are gearing up to enter the field.

“There is a lot more demand for loans but very little supply,” said Richard Beleutz, CEO Alternative Investment Resource, a Chicago-based investment company.

In the last two years, “there is a large and growing set of asset managers looking to directly provide funding to consumers,” said Nathan Popkins, CEO of a Chicago-based lending company Cumulus Funding.

Alternative lending tends to grow when strict banking regulations are in place, as investors search for higher returns, according to an International Monetary Fund report on alternative banking.

There’s plenty of growth left in the P2P marketplace. “Alternative lenders only address a small fraction of trillion dollars of need in America,” said Alternative Investments’ Beleutz.

To consumers, non-bank loans are attractive alternatives to traditional bank loans and a way to refinance their debt. “Fifty percent of Americans only have 3 month worth of expenses in liquid asset they have access to,” said Popkins.

Most credit-seekers simply do not have the credit score required for desirable bank loans. These borrowers are generally considered “subprime,” or less desirable, candidates

After the credit crunch in 2008, only pristine-rated borrowers can get loans from banks, noted David Min, Assistant Professor of Law at University of California Irvine and a financial market regulation expert.

“Subprime borrowers are out there, with different income and color, but they still need credit,” said Min, former staff attorney at the Security and Exchange Commission.

They’re paying up for the privilege: Lending Club breaks down borrowers into several different risk categories, but only 14.4 percent of its borrowers are top grade, according the company’s website. Because so many of its clients are lower-ranked, for the last quarter, Lending Club charged an interest rate of 14.1 percent on average.

Top grade borrowers enjoy rate as low as six to eight percent, while the worst grade consumers are charged more than 26 percent.

Even though interest rates are high, direct lending has gained popularity in recent years.

Individuals on contract income are not eligible for loans. People on non-employment income often get penalized for getting bank loans.

Others who do not own enough assets are generally less likely to obtain loans.

Offline versions

Alternative lending is not limited to online, nationwide platforms. Smaller non-bank lenders have hurried in the last few years to enter this exponentially growing consumer finance market.

Like Lending Club, they take in investments and lend money to borrowers, and they are not restricted by regulations and supervision that regular banks have.

Small investors and low profile pledgers often feel disadvantaged on national levels to compete for the best deals. Hence, the rise of local alternatives is inevitable.

Cumulus Funding, a Chicago-based lender, engages in the private finance market by lending money to individuals based on an income share agreement.

Borrowers pay Cumulus a fixed percentage of their income instead of paying installments, said the firm’s CEO Popkins. Because Cumulus does not specify a fixed interest rate, the company has the potential to get more than what it could get from a fixed interest rate.

If the borrower makes more money than when he or she signed the contract, Cumulus makes more money since the lender is taking the same percentage of the increased income.

Borrowers’ credit scores will not be adversely affected even if they could not make a full payment on time due to reduced wages or sudden unemployment. They simply pay less if their salaries are reduced.

Other lenders have different loan products to suit consumer needs.

Effective interest rate for a typical loan from small alternative lenders could reach 40 percent, depending on the credit history of customers, according to Cumulus’ lending formula. This is significantly higher than Prosper and Lending Club or typical loan.

The IMF has called for more oversight on the alternative investment practices of private lenders.

“There is nothing inherently wrong with lending money to subprime borrowers. People have bad time and they still need credit,” said Min. But, he added, “Many financial firms start to target these borrowers often on predatory terms.”

Consumer credit activities are regulated at state level. And the alternative-loan sector has generated its share of friction.

In Illinois, customers of these lenders filed thousands of complaints. In the first ten months of this year, more than 650 cases have to do with inaccurate database information or unofficial financial documents provided by lenders to qualify obligors for loans, according to monthly reports compiled by the Illinois Department of Financial and Professional Regulation.

About 60 cases in Illinois involve interest rate miscalculation or manipulation, based on the same source.

“Too many quasi-financial intermediaries are lenders. And they are not supervised by banking regulators,” opening the door to possible abuses, said Scott Fearon, hedge fund manager.

However, it is still too early to tell if alternative lending will have a negative effect on the economy, explained Min.

Despite such growing pains, the P2P lenders have tremendous space “to expand into a market with seemingly endless demand,” said Beleutz.